IN an emerging and growing economy like India, we need to maintain a healthy investment rate to increase gross capital information. Obviously such investment can not be raised domestically as the resources and savings are limited. Therefore, to do it, we need to attract, long term FDI in plant, machinery and productive assets, popularly called as sticky FDI. To attract Foreign Direct Investment (FDI) in an era of intense global capital reallocation and geopolitical fragmentation, a country must transition from merely offering a large consumer market to providing an efficient, predictable, and globally integrated production base and decent return on investment. It may be stated that major source countries for FDI are Singapore, Mauritius, USA, Netherlands and Japan, while the destination is Maharashtra, Gujarat, Karnataka and Delhi. Further major investment is going to Computer software and hardware and services sector, with significant amount flowing to Semi Conductors, Electronics, Auto and real estate.

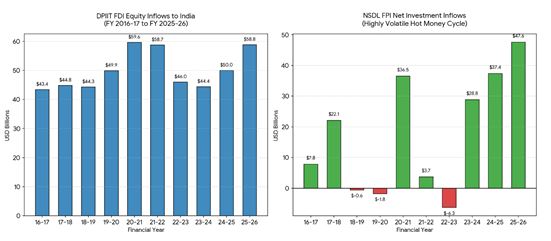

The massive wave of Foreign Institutional Investor (FII) and Foreign Portfolio Investor (FPI) outflows from the Indian market in 2026, as also the year before has been one of the biggest stories on Dalal Street. In fact, March 2026 saw the sharpest single-month FII sell-off on record. Foreign Portfolio Investors (FPIs) withdrew record amounts from Indian equities. In fact in the financial year 2025-26, they pulled out approximately Rs.1.66 lakh crore. The exodus accelerated severely in 2026-27, with FPIs divesting a further Rs.2.87 lakh crore from Indian equities in just the first few months of the financial year, putting too much pressure on rupee. Interestingly rupee depreciated by over 10%, over last 12-15 months, because of huge money leaving abroad. The net FDI also reduced to just 340 million during 2024-25 and about 7.7 Billion in 2025-26, even though gross FDI figures were significantly higher at $94.53 billion, which included FDI equity inflows of $ 58.85 Billion and rest retained earnings which were reinvested in expansion etc., by the foreign investors. The RBI breaks down the massive structural outflows that reduced the final Net FDI retention to just USD 7.65 billion, as below:

|

Gross Inflow / Outflow Component

|

Amount (FY 2025-26)

|

Operational Impact on Indian Capital

|

|

Gross FDI Inflows

|

(+) USD 94.53 Billion

|

Total physical foreign capital entering the economic borders.

|

|

Repatriation & Disinvestments

|

(-) USD 53.58 Billion

|

International private equity firms booking profits and exiting through India's deep IPO markets.

|

|

Outward FDI by Indian Firms

|

(-) USD 33.29 Billion

|

Indian corporations aggressively investing capital overseas to expand their global footprints.

|

|

Net FDI Inflow Balance

|

(=) USD 7.65 Billion

|

The actual long-term net capital added to India's Balance of Payments (BoP).

|

The statistics of FDI/FPI/Inward remittances for the last ten years is presented below:

|

Year (Fiscal/Calendar)

|

Gross FDI Inflows

|

FPI Net Investment

|

Inward Remittances

|

|

2016-17

|

$60.2 B

|

$7.8 B

|

$68.9 B

|

|

2017-18

|

$61.0 B

|

$22.1 B

|

$69.0 B

|

|

2018-19

|

$62.0 B

|

-$0.6 B

|

$76.4 B

|

|

2019-20

|

$74.4 B

|

-$1.8 B

|

$83.2 B

|

|

2020-21

|

$81.7 B

|

$36.5 B

|

$80.2 B

|

|

2021-22

|

$83.6 B

|

$3.7 B

|

$89.1 B

|

|

2022-23

|

$71.0 B

|

-$6.3 B

|

$101.7 B

|

|

2023-24

|

$70.9 B

|

$28.8 B

|

$106.6 B

|

|

2024-25

|

$81.0 B

|

$37.4 B

|

$135.4 B

|

|

2025-26

|

~$94.53 B

|

~$47.6 B

|

$144.7 B

|

Source : RBI Statistics 2025-26

The DPIIT also periodically prepares details of such investments in the country and statistics prepared by it shows interesting trends over last few years. It appears that such investments peaked in post covid period in 2020-21 and 2021-22 but later lost steam. Once again it picked up in FY 2025-26. As per world bank also, India foreign direct investment for 2024 was $ 27.14 billion, a 3.37% decline from 2023, while in 2023 it was $ 28.09 billion, a 43.76% decline from 2022. On the other hand in 2022, it was 49.94 billion US dollars, a 11.66% increase from 2021. In the same vein, in 2021, it was 44.73 billion US dollars, a 30.51% decline from 2020. The foreign direct investment refers to direct investment in equity flows in the reporting economy. It is the sum of equity capital, reinvestment of earnings, and other capital. Direct investment is a category of cross-border investment associated with a resident in one economy having control or a significant degree of influence on the management of an enterprise that is resident in another economy. Ownership of 10 percent or more of the ordinary shares of voting stock is the criterion for determining the existence of a direct investment relationship.

Even though India's domestic sector is strong with GDP Growth of over 7.7% during FY 2025-26, with inflation and Fiscal deficit under control and bank balance sheets being robust, the external sector, Balance of Payment and current account balance is showing bit of strain, because of war in middle east, as also foreign capital leaving the shores, as US bond market is showing better returns. Now Let's discuss the structural framework required to attract sticky foreign capital, the latest policy pivots India has made in 2025-2026, and recently and a critical assessment of their sufficiency.

The Core Framework: How to Attract FDI

Attracting long-term foreign capital requires moving beyond tax arbitrage and focusing on structural enablers:

- Policy Predictability: Global boardrooms base billion-dollar capacity expansion decisions on 10-year timelines. They require absolute certainty regarding tax regimes, tariff structures, and data protection rules without the threat of retrospective changes. The recent tax ruling in the case of Tiger Global has sent some disturbing signals to the foreign investors whose memory of Vodafone PLC and Cairns India tax matter is still fresh.

- Factor Market Competitiveness: Seamless access to affordable industrial land and flexible labor markets are non-negotiable for large-scale manufacturing FDI. Though India has liberalised the labour laws still implementation on the ground is an issue. The land acquisition is still a problem at most of the places, being a state subject.

- Integration into Global Value Chains (GVCs): Modern manufacturing is highly fragmented. To attract a smartphone assembler, a country must allow the frictionless, low-tariff import of the requisite intermediate components, as also creating an ecosystem to manufacture such components within the country to add more value.

- Ease of Doing Business (EoDB) 2.0: Shifting the focus from federal-level statutory clearances to state-level and municipal execution, including contract enforcement and dispute resolution timelines.

Policy Interventions by India (2025-2026)

India has recently recognized that its macroeconomic stability alone is not enough to secure capital in a volatile global system. In early 2026, the government initiated a series of highly pragmatic, calibrated policy shifts:

The Strategic Easing of Press Note 3 (March 2026): This is the most significant recent pivot. Initially implemented in 2020 to curb opportunistic takeovers from Land Bordering Countries (LBCs) like China, the strict PN3 rules created bureaucratic bottlenecks for global private equity funds with even minor Chinese backing. The Government amended the policy to allow investors from LBCs with up to 10% non-controlling beneficial ownership to invest via the automatic route. A strict 60-day approval timeline was introduced for critical manufacturing sectors-specifically electronic components, capital goods, solar cells, and polysilicon. India is strategically allowing controlled Chinese capital and technology to enter the country to build domestic manufacturing capacity and value addition.

Defining "Beneficial Ownership": The 2026 FDI SOPs formally tied the definition of beneficial ownership to the Prevention of Money Laundering Act (PMLA) thresholds. This removes regulatory ambiguity that previously stalled complex cross-border venture capital and private equity deals.

Sectoral Liberalization: Following prolonged consideration, the Sabka Bima Sabki Raksha Act of 2025 successfully permitted 100% FDI in the insurance sector, fully opening a traditionally capital-starved financial pillar to global players.

Sustained Supply-Side Push: Production-Linked Incentive (PLI) schemes continue to be expanded, generating over $24 billion in domestic and foreign investments by late 2025, heavily targeting electronics, pharmaceuticals, and automobiles.

Recent Steps taken by RBI and the Government to Shore up Foreign Investment:

To address recent capital outflows and stabilize the rupee, the Reserve Bank of India (RBI) and the Indian government recently announced a comprehensive package of measures in June 2026 aimed at attracting foreign investment and shoring up foreign exchange reserves. The details of of the key steps taken across different sectors are as follows:

1. Easing Foreign Investment in Government Securities (G-Secs)

The RBI and the government have made significant regulatory and tax changes to make Indian debt markets more attractive to Foreign Portfolio Investors (FPIs):

- Tax Exemptions: The government issued an ordinance, exempting foreign investors from paying taxes on interest income and capital gains on the transfer, sale, or exchange of G-Secs, applied retrospectively from April 1, 2026.

- Expansion of the Fully Accessible Route (FAR): The RBI has expanded the universe of "specified securities" under the FAR. Foreign investors can now freely invest in new issuances of G-Secs and sovereign green bonds with longer tenors of 15, 30, and 40 years, in addition to the previously permitted 5, 7, and 10-year tenors.

- Removal of FPI Restrictions: Under the General Route, the RBI has removed several compliance barriers for FPIs investing in G-Secs, including short-term investment limits, security-wise limits, and concentration limits. Furthermore, the 'general' and 'long-term' sub-categories of investment limits have been merged into a single consolidated limit to provide greater flexibility.

Broadening Access to Equity Markets

Steps were also taken to encourage direct investments in listed Indian stocks by non-residents. The Foreign Exchange Management Act (FEMA) rules were amended to allow all individual Persons Resident Outside India (PROIs) to invest in equity instruments through the portfolio investment scheme-a facility previously restricted mainly to Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) without SEBI registration. Further individual PROIs can now invest up to 10% in a single company (raised from 5%), and the overall aggregate investment limit for these individuals has been raised to 24% (up from 10%).

Incentivizing Banking Deposits and Foreign Borrowing

To bring in fresh dollars and manage the costs associated with currency risks, the RBI introduced specific concessions for banks and public sector enterprises. To encourage the inflow of foreign currency, the RBI has fully exempted fresh 3-to-5-year Foreign Currency Non-Resident (Bank) deposits from Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements until the end of September 2026. Additionally, the RBI will bear the full foreign exchange hedging costs for authorized banks raising these deposits. The RBI is also providing a concessional forex swap facility until September 30, 2026, to incentivize Public Sector Undertakings (PSUs) to raise funds through ECBs.

Expert Assessment: Are These Steps Enough?

The recent calibrations are highly necessary and signal a shift from defensive protectionism to confident economic pragmatism. However, from a structural standpoint, they are arguably insufficient on their own to engineer a massive, sustained manufacturing renaissance. While federal policy has created the enabling architecture, the actual absorption of FDI faces severe ground-level friction:

A. The Execution Bottleneck (State vs. Center)

Easing FDI caps and federal rules (like the PN3 amendment) looks excellent on a regulatory dashboard, but capital hits the ground at the state level. Land acquisition, localized bureaucratic inertia, utility connections, and municipal environmental compliances remain deeply complex. An investor looking to build a multi-acre facility still faces a labyrinth of sub-national red tape.

B. Factor Market Rigidities

Capital naturally flows to where labor is highly productive and regulations are adaptable. While the historic consolidation of labor laws into four central Labor Codes was a monumental legislative victory, the actual on-ground implementation, harmonization of state-level rules, and enforcement mechanics remain a work in progress in 2026. Until labor flexibility is realized on the factory floor, large-scale, labor-intensive manufacturing FDI will hesitate.

C. The Tariff and Trade Paradox

Attracting FDI into manufacturing is fundamentally linked to export competitiveness. While India is actively pursuing early-stage CEPAs to open new markets, it simultaneously maintains relatively high import tariffs on certain intermediate goods to protect domestic industries. A country cannot easily become a global export hub if it is prohibitively expensive to import the components needed to build the final product.

Thus recent steps taken by the Government and the RBI to attract foreign investment, particularly the nuanced handling of LBC capital to secure advanced electronic and semiconductor supply chains, are excellent macroeconomic maneuvers. They resolve a major bottleneck for global funds. However, they alone may not be sufficient to attract major investment and some more steps may be needed including some tweaking in tax provisions relating to long term capital gains on equity investments and tax withholding provisions relating to that. To translate this theoretical capital into physical factories, the next phase of reform must rigorously focus on state-level execution, the stabilization of tariff regimes, and the smooth roll out of the labor reforms at state level.

( About Author : Mr. Pratap Singh is an IRS Officer with over 35 years experience of working at senior positions in Government across India. He is a trained Civil Engineer and holds M. Tech Degree in Civil Engg from IIT Kanpur. He worked as Asstt. Executive Engineer(Civil) in the Government and led important projects, before joining IRS.)

[The views expressed are strictly personal. AI has not been used to generate any part of this content. ]

|